Fear is not symmetric¶

Fear is not symmetric. The fall is longer than the rise. In 1987 this was made plain, and the vol surface has remembered ever since.

Term structure describes how IV varies across expiries. Skew describes how IV varies across strikes at a single expiry. Black-Scholes assumes a single \(\sigma\) prices every strike; observed market prices depart from that assumption, and the shape of the departure carries information.

Characteristic shapes¶

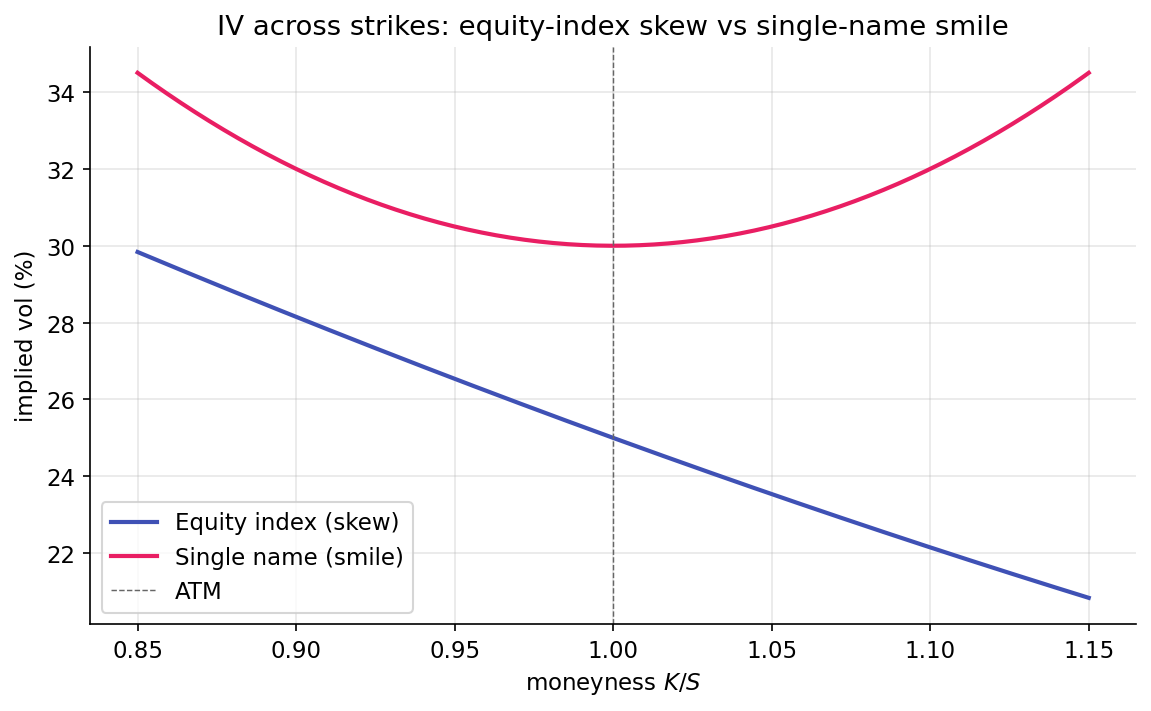

Plot ATM IV, OTM put IVs, and OTM call IVs for SPX and for a single name at a matched 30-day expiry. Two characteristic shapes appear:

For the equity index, OTM puts trade at higher IV than ATM, and ATM trades at higher IV than OTM calls. The curve slopes downward in strike — the classic equity-index skew. Single-name equities often show a different shape, with IV elevated on both wings, producing a smile.

The index remembers crashes. The single name remembers earnings, takeovers, announcements. The shapes differ because the memories differ.

The historical origin¶

Before October 1987, the IV surface was approximately flat across strikes. After the crash, this changed. Participants concluded that large downside moves occurred more frequently than Black-Scholes (log-normal tails) predicted, and demand for OTM put protection rose. That demand has not fully subsided.

Dealers now quote OTM puts at a premium that reflects the persistent hedging bid and the perceived fat left tail. Every equity index has carried skew since. It is the market's way of saying: we have not forgotten.

The asymmetry has a second cause. Leverage effect: when stocks fall, implied leverage rises (same debt, smaller equity), increasing equity risk. Realized volatility tends to rise on large down moves and fall on large up moves. Stochastic volatility models with negative return-volatility correlation naturally produce a skewed implied-volatility surface.

The 25-delta skew measure¶

Many measures quantify skew. The most common in practice, and the one this project uses:

A 25-delta put is an OTM put with delta \(-0.25\). A 25-delta call is the corresponding OTM call with delta \(+0.25\). The skew is the spread between their IVs.

For a typical equity index in calm markets, this spread is in the 2–4 vol-point range. In stressed conditions, it widens to 6–10 points. In euphoric regimes where short-volatility strategies are complacent, it can compress toward zero.

A flat skew often precedes volatility events. When the market stops paying for protection, the storm is near.

The 25-delta convention is a compromise: far enough OTM to lie in the insurance region of the distribution, close enough that liquidity supports reliable IV quotes.

Delta-space interpolation¶

Option chains do not quote strikes at fixed delta values — they quote at fixed prices (for example, 400, 405, 410). Computing IV at exactly 25-delta requires interpolation. The standard method: map each quoted strike to its delta (using Black-Scholes with the strike's own IV), then interpolate IV across the delta axis.

Working in delta-space rather than strike-space is intentional. The 25-delta point on SPX moves with \(S\), so the skew measure remains in the same part of the risk distribution regardless of where spot sits today. Strike-based measures conflate spot moves with skew moves.

The implementation in skew.py walks the chain, computes each contract's delta, and linearly interpolates IV at the target delta. Linear interpolation is adequate for normally-shaped surfaces; for more accurate tail-shape fits, SABR or SVI parameterizations are standard alternatives.

Skew z-score as a regime input¶

Raw skew levels matter less than their position relative to their own history. A rolling z-score captures this:

Three regions of \(z_\text{skew}\) are informative:

- Highly positive \(z\): skew is historically steep. Puts are expensive relative to history. Either priced-in stress, or aggressive hedging ahead of an anticipated event.

- Near-zero \(z\): skew is at its historical norm. No signal on this axis.

- Highly negative \(z\): skew is flattening or inverting. Put protection is unusually cheap relative to history. This condition often precedes volatility events.

When hedgers stop paying for protection, or when active selling compresses the spread — we should look up from our screens.

The regime classifier uses a negative threshold on \(z_\text{skew}\): when the z-score is deeply negative (default threshold \(-2.0\)), the condition triggers a short-gamma regime tag.

When skew fails as a signal¶

Two recurring cases in which skew movement is uninformative:

- Earnings season for single names: pre-earnings skew shifts reflect the upcoming event, not a structural regime change. Index skew is less affected.

- Dealer inventory rebalancing: large customer orders can move individual strike IVs without signaling anything about market risk tolerance.

The regime classifier mitigates the first case by using index-level (SPX) skew, where idiosyncratic effects are diluted.

Smile versus skew — parameterizing the surface¶

For a complete treatment, practitioners fit parametric models across strikes and expiries:

- SVI (Stochastic Volatility Inspired): five parameters per expiry, fit to strike-IV pairs. Fast, common in risk systems.

- SABR: four parameters including a \(\beta\) that controls whether the surface is skew-like or smile-like. Common in FX and rates.

The regime classifier does not require a parametric fit: the 25-delta skew is a scalar summary that captures sufficient surface asymmetry. Future strategies requiring finer-grained information could extend to SVI or SABR.

Summary¶

- The equity-index IV surface slopes downward in strike (skew); single-name surfaces often form a smile. Different customer flow patterns, different structural risks.

- Skew is measured in delta-space rather than strike-space because delta moves with spot, producing a measure invariant to the current market level.

- Flattening of skew, rather than steepening, often precedes volatility events — it reflects complacency about downside risk.

Implemented at¶

trading/packages/gex/src/gex/skew.py:

- Line 26:

interpolate_iv_at_delta(chain, target_delta, option_type, spot, rate)filters to the shortest expiry with ≥21 DTE, maps each contract to its delta, linearly interpolates IV at the target delta. - Line 64:

skew_25d(chain, spot, rate)computes the scalarIV(25d put) - IV(25d call).

The regime classifier in regime.py:classify_regime consumes skew_25d_z (the rolling z-score of daily skew) and triggers the short-gamma regime when z ≤ -2.0.

Fear is not symmetric. The market remembers what hurt it. Next: who stands opposite each trade.